Legal Issues Pertaining to Sweeping

Legal Issues Pertaining to Sweeping |

|

Recover Loss of Revenue – and More – After "Not-at-Fault" Accidents

by Brian J. Ludlow and Ranger Kidwell-Ross When your vehicles get hit by a third party, their insurance is liable not only for the physical damage, but also the lost revenue and use while the unit is being repaired.

Let's begin with the steps that should be taken to help recover the maximum from your not-at-fault accidents when one occurs.

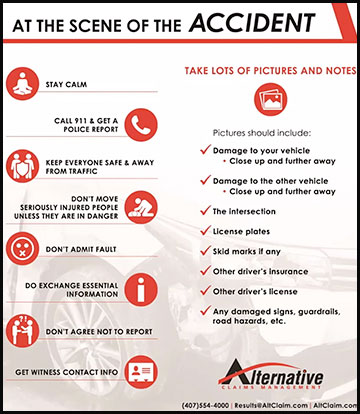

1. Taking lots of pictures is the single best advice we can give. A picture may be worth 1,000 words, but when it comes to accidents, a picture can be worth thousands of dollars. Take pictures of the accident scene, damage to both units, license plates, skid marks, debris, path of final resting place of the vehicle, third-party driver's license and insurance information.

What Am I Entitled to From a "Not-at-Fault" Accident?Although some states have specific language on what is recoverable, essentially you are entitled to your physical damage, cost for transporting the damaged unit, Loss of Revenue (LOR) or Loss of Use (LOU) and Diminution of Value (DV). How much you are entitled to depends on several factors and are the subjective negotiations that damage recovery firms engage in hundreds of times each day. You can typically pursue claims up to six years old, although this depends on your state statute of limitations, in order to recover Loss of Revenue/Use on old claims. Pursuing Loss of Revenue or Loss of Use

The following are steps you can take to help maximize recovery: Getting accurate value when a vehicle is a total loss.The term "Total Loss" is an insurance term lacking legal definition. Carriers have often used title branding laws to determine if a vehicle is a "Total Loss." While each state has different criteria for "branding" titles, vehicles can and have been paid as total losses with damage percentages well below the title branding statutes. Carriers often tout statements such as "Federal Guidelines" or "State Statutes" when attempting to settle claims. More accurately, legal entitlements are based upon what is called the Restatement of Torts and defined by case law in each state. Engaging a firm that specializes in commercial fleet claims can provide an arm's length transaction necessary to be proactive on the front side in setting the claim up properly, which usually results in a higher recovery. So how do you win at the recovery game? Unfortunately, you are in a game where the opponent is motivated to deny or delay your claim and defend their insured. Persistence, knowledge of the law and industry, plus proper supporting documentation is key to winning.

There are essentially three routes for recovering "not-at-fault claims".

1. Handle the claims yourself. Unless you have extensive knowledge of the law and insurance industry, plus have ample time to talk to the voicemails of insurance carriers this option may not be ideal and detract from your core business.

Keep This Form in Your Company VehiclesThe form you see to the right provides handy access to what your operator needs to know – and remember to do – whenever an accident occurs. Although the advice used to be to put a camera into each vehicle, today everyone has a cell phone that can be used to take the needed photos, including of the other party's driver's license, insurance card, etc. Click onto the small image to access a PDF file of the same information in a format that is suitable for printing onto card stock so as to have the info placed into your vehicles.

The following 40-minute Zoomcast seminar by Brian Ludlow discusses the above concepts in detail. Click on the image below to access; we highly recommend watching it.

Brian J. Ludlow is Executive Vice President for Alternative Claims Management. He was the former president of an insurance company and is now a consultant to the insurance, financial and transportation industries, including power sweeping and pavement management. His goal has been to transform the fleet damage recovery process.

|

© 2005 - 2022 World Sweeper

|

Legal Issues Contents

|